Summary

- Take control of high-interest debt by consolidating multiple payments into one manageable monthly payment with Lotly's secured home loan process.

- Access funds quickly and efficiently without the typical roadblocks of traditional banking. Lotly welcomes all credit scores and income types, including self-employed and gig workers.

- Protect your financial future by making strategic decisions about your home equity, especially during periods of prime rate volatility.

- Get personalized solutions that fit your unique financial situation, not one-size-fits-all products that may not address your specific needs.

The prime rate is the invisible force that shapes your mortgage payments, credit card interest, and overall borrowing costs. Currently sitting at 4.45% (as of November 2025), this benchmark rate influences virtually every loan in your financial portfolio.

Understanding the prime rate isn't just for economists or bankers. It's essential knowledge for:

- Homeowners with variable-rate mortgages who want to predict future payment changes

- Borrowers looking to consolidate high-interest debt in a fluctuating rate environment

- Prospective buyers trying to determine the best time to enter the market

When the Bank of Canada makes an announcement, your financial future hangs in the balance. Let's unpack what the prime rate really means for your wallet and how you can navigate its changes strategically.

By the way — prime is down. Are your borrowing costs following? Lotly reviews your home-equity options against today’s rate environment and your full financial picture — including income sources traditional lenders skip over. Book a free consultation to see if you’re sitting on untapped cash today.

What is the prime rate in Canada?

The prime rate in Canada is the benchmark interest rate that banks and other financial institutions use as a foundation for pricing their variable-rate loans and lines of credit. It serves as an "anchor rate" from which other interest rates are calculated, typically by adding or subtracting a percentage.

Unlike what many believe, the prime rate isn't set by the government or the Bank of Canada directly. Each financial institution sets its own prime rate, though the major banks typically move in unison. What we commonly refer to as "Canada's prime rate" is actually (unofficially) the statistical mode of the rates posted by the six largest banks, as calculated by the Bank of Canada.

Think of the prime rate as the starting point for negotiations between lenders and borrowers. When you see a loan advertised as "prime plus 0.5%" or "prime minus 0.25%," that's the lender telling you how your interest rate relates to their prime rate.

Current prime rate in Canada

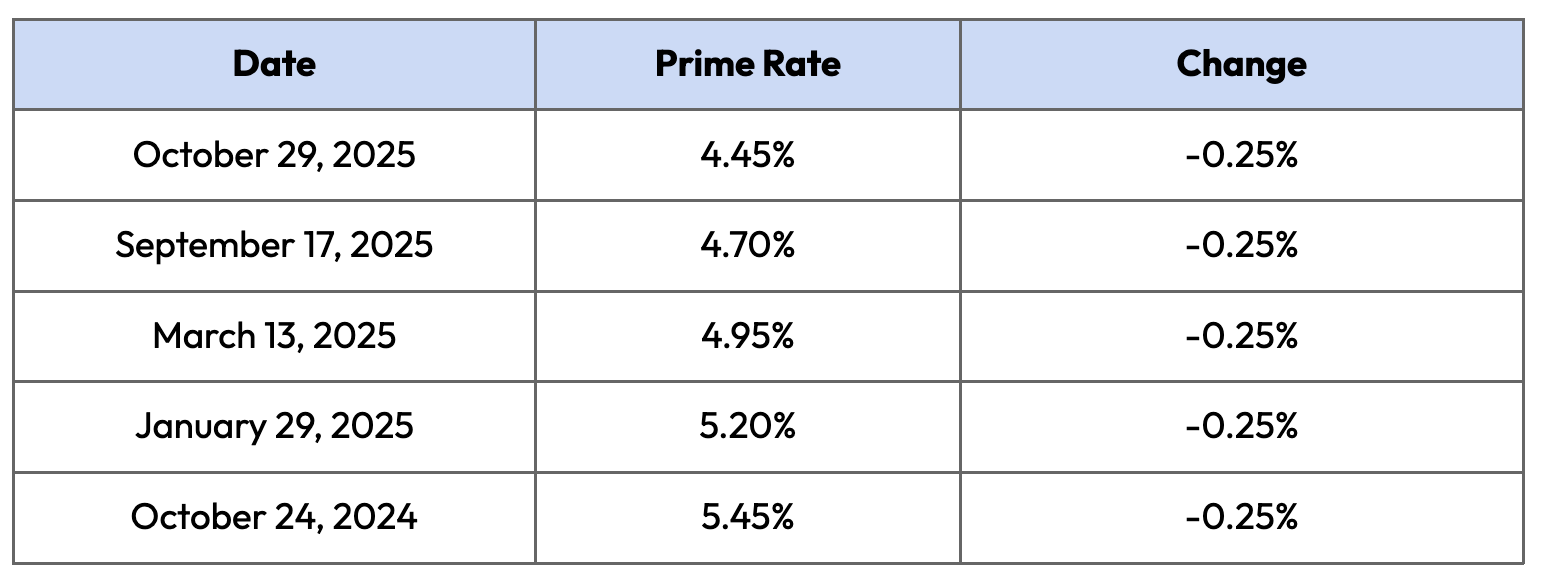

As of November 2025, Canada's prime rate sits at 4.45%. This rate reflects the most recent change on October 29, 2025, when banks lowered their prime rates by 0.25 percentage points from 4.70% to 4.45%.

Here's how the prime rate has changed over the past year:

This downward trend reflects the Bank of Canada's efforts to ease monetary policy as inflation has stabilized, providing some relief to variable-rate borrowers after the steep increases seen in 2022-2023.

How is the prime rate determined?

The prime rate doesn't exist in a vacuum—it's directly influenced by the Bank of Canada's overnight rate. When the central bank adjusts its policy rate, commercial banks typically respond by adjusting their prime rates accordingly.

Banks generally maintain a spread of approximately 2.20 percentage points above the Bank of Canada's overnight rate. For example, with the current overnight rate at 2.25%, the prime rate is 4.45%, maintaining a 2.20% spread.

This relationship isn't legally mandated but has remained remarkably consistent over time. Banks maintain this spread to cover their operating costs, risk premiums, and profit margins while remaining competitive in the market.

While each bank technically sets its own prime rate independently, competitive pressures mean that when one major bank adjusts its prime rate, others typically follow within hours or days. This is why we can generally speak of "Canada's prime rate" as though it were a single number.

Historical trends of Canada's prime rate

Canada's prime rate has taken borrowers on a wild ride over the decades, from sky-high rates that made homeownership nearly impossible to historic lows that fueled housing booms.

Looking back at this financial rollercoaster provides valuable context for understanding today's rate environment and where we might be headed next. The prime rate's history isn't just a collection of numbers—it's a reflection of Canada's economic journey through inflation crises, recessions, global financial turmoil, and periods of growth.

Early 1980s: the peak

The early 1980s saw Canada's prime rate reach a staggering 22.75% in August 1981—a number that seems almost unbelievable today. This extreme was driven by the Bank of Canada's aggressive fight against runaway inflation, which had reached double digits. Mortgage rates above 20% effectively froze the housing market and pushed many borrowers into financial distress.

2008-2009: financial crisis response

During the global financial crisis, the Bank of Canada slashed its overnight rate to support the economy. The prime rate followed suit, reaching 2.25% in April 2009 — which was then considered an extraordinary low. This dramatic reduction helped cushion the Canadian economy from the worst effects of the global recession.

2020: pandemic lows

When COVID-19 struck, the Bank of Canada took emergency action, cutting rates rapidly. By March 2020, the prime rate had fallen to a historic low of 2.45%, where it remained for an extended period. This unprecedentedly low rate supported the economy through lockdowns and helped fuel a surprising housing boom despite the pandemic.

2022-2023: inflation fighting

As post-pandemic inflation surged, the Bank of Canada responded with one of the fastest rate-hiking cycles in its history. The prime rate climbed from 2.45% to 7.20% in just 18 months, putting significant pressure on variable-rate borrowers and cooling the housing market.

2024-2025: gradual easing

With inflation finally coming under control, 2024 and 2025 have seen a series of measured rate cuts, bringing the prime rate down to its current level of 4.45%. This gradual easing has provided relief to borrowers while maintaining the Bank's credibility in its fight against inflation.

These historical periods demonstrate how the prime rate responds to economic conditions and central bank policy—and how dramatically it can affect borrowers' financial situations.

How the prime rate affects your finances

The prime rate isn't just a number for the financial analysts track — it has real, tangible impacts on your day-to-day finances and long-term economic health. When the prime rate changes, the effects ripple through nearly every aspect of your financial life.

Understanding these connections helps you make smarter decisions about borrowing, saving, and managing debt. Let's explore how changes in the prime rate flow through to various financial products and ultimately to your wallet.

Impact on mortgages and home loans

Variable-rate mortgages are directly tied to the prime rate, typically quoted as "prime plus/minus" a percentage. For example, a competitive variable mortgage might be priced at "prime minus 0.50%." With today's prime rate at 4.45%, that mortgage would have an effective rate of 3.95%.

When the prime rate changes, your variable mortgage rate changes with it, affecting either your payment amount or your amortization period, depending on your mortgage structure:

Variable-rate mortgage with fixed payments: If you have a variable-rate mortgage with fixed payments (common in Canada), a prime rate increase means more of your payment goes toward interest and less toward principal. This extends your effective amortization period without changing your monthly payment.

For example, on a $500,000 mortgage with a 25-year amortization and a rate of prime minus 0.50%:

- At prime = 4.45% (effective rate 3.95%): Monthly payment = $2,621

- Interest portion: $1,646

- Principal portion: $975

- If the prime increases to 4.95% (effective rate 4.45%): Monthly payment remains $2,621

- Interest portion: $1,854 (+$208)

- Principal portion: $767 (-$208)

This "payment allocation shift" means you're building equity more slowly. Over five years, this 0.50% rate increase would result in approximately $12,500 less equity in your home—money that essentially disappears into interest payments.

Variable-rate mortgage with variable payments: If your variable mortgage has adjustable payments, your monthly payment will increase or decrease directly with prime rate. This maintains your original amortization schedule but affects your monthly cash flow.

Fixed-rate mortgages, by contrast, are unaffected by prime rate changes during their term. However, at renewal time, the prevailing rates (which are influenced by the prime rate trend) will determine your new payment amount.

Effect on other loans and credit products

The prime rate's influence extends far beyond mortgages:

- Home Equity Lines of Credit (HELOCs): These are typically priced at prime plus 0.50% to prime plus 1.00%. When the prime rate changes, your HELOC interest rate adjusts immediately, affecting your minimum payment and interest costs.

- Personal Lines of Credit: Similar to HELOCs, personal lines of credit are usually priced at prime plus a premium (often 2-7% depending on your credit profile). Rate changes affect your borrowing costs immediately.

- Credit Cards: Many credit cards have variable rates tied to the prime rate. When the prime increases, your credit card interest rate typically rises by the same amount, making carrying a balance even more expensive.

- Car Loans: While many car loans are fixed-rate, variable-rate auto financing is also available and tracks the prime rate.

- Student Loans: Government student loans often have a variable-rate component tied to prime, so rate changes can affect your payment or amortization period.

For Canadians carrying multiple forms of debt, prime rate increases can compound, significantly impacting monthly cash flow. This is why many borrowers consider debt consolidation strategies when rates are rising.

Prime rate vs. Bank of Canada overnight rate

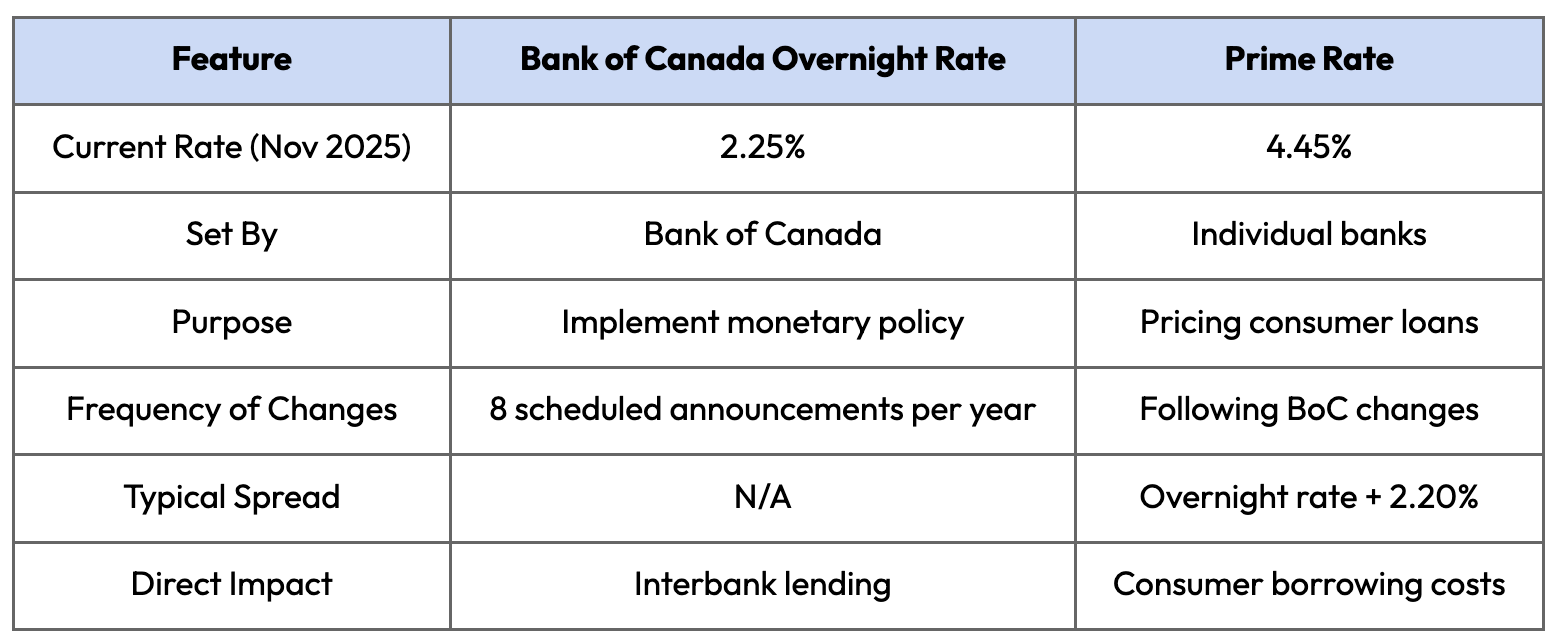

While often mentioned together, the Bank of Canada overnight rate and the prime rate serve different functions in the financial system. Understanding their relationship helps you better interpret economic news and anticipate how policy changes might affect your personal finances.

The Bank of Canada overnight rate (also called the policy rate) is the interest rate at which major financial institutions borrow and lend one-day (or "overnight") funds to one another. It's the primary tool the Bank of Canada uses to implement monetary policy and influence economic activity.

The prime rate, as we've discussed, is the benchmark rate that banks use to set interest rates for variable-rate loans and lines of credit offered to consumers and businesses.

Here's how they compare:

When the Bank of Canada changes its overnight rate, banks typically adjust their prime rates within hours or days. The standard practice is to maintain a spread of approximately 2.20 percentage points above the overnight rate, though this can occasionally vary.

For example, when the Bank of Canada cut its overnight rate by 0.25% on October 29, 2025 (from 2.50% to 2.25%), the major banks followed by reducing their prime rates by the same amount (from 4.70% to 4.45%).

This predictable relationship means that borrowers can generally anticipate prime rate changes by watching the Bank of Canada's monetary policy announcements and economic outlook statements.

Managing your finances during prime rate changes

Prime rate fluctuations can significantly impact your financial situation, but with proper planning and strategic decision-making, you can minimize adverse effects and even take advantage of changing rate environments.

Whether rates are rising or falling, having a proactive approach rather than simply reacting to changes can make a substantial difference in your financial well-being. Here are strategies to consider for different rate scenarios.

When to consider debt consolidation

Rising prime rates can quickly increase the cost of carrying multiple debts, especially high-interest credit cards, lines of credit, and variable-rate loans. This is often the perfect time to consider debt consolidation.

Debt consolidation makes particular sense when:

- You're carrying multiple high-interest debts with rates that keep climbing

- The spread between secured loan rates and unsecured debt rates is widening

- Your monthly payments are becoming difficult to manage

- You have sufficient home equity to qualify for a secured loan

How to approach debt consolidation effectively:

- Calculate your total debt load across all accounts, noting the interest rate on each

- Determine your home equity by subtracting your mortgage balance from your home's current market value

- Compare potential savings between your current situation and a consolidated loan

- Consider secured home loans that use your equity to provide lower rates

Lotly's secured home loans have helped Ontario homeowners consolidate multiple high-interest debts into one manageable payment, often at a lower rate. This approach can free up cash flow and reduce financial stress, especially when variable rates are climbing.

For example, if you're carrying $50,000 in credit card debt at 19.99% and a $20,000 line of credit at prime plus 3% (currently 7.45%), your monthly interest cost alone is over $1,000. Consolidating with a secured home loan at a lower rate could save you hundreds of dollars a month while simplifying your finances.

When evaluating debt consolidation options, look beyond just the interest rate. Consider:

- The total cost over the life of the loan

- Any fees or charges for setting up the new loan

- The impact on your monthly cash flow

- Whether you'll actually close the high-interest accounts after consolidating

Fixed vs. variable: making the right choice

The decision between fixed and variable rates is one of the most important choices borrowers face, and it becomes even more critical during periods of prime rate volatility.

When variable rates might make sense:

- When prime rates are falling or expected to fall

- When the spread between fixed and variable rates is unusually large

- When you have financial flexibility to handle potential rate increases

- When your time horizon is relatively short

When fixed rates might be preferable:

- When prime rates are rising or expected to rise

- When the spread between fixed and variable rates is small

- When you need payment certainty for budgeting

- When your risk tolerance is low

Assessing your personal risk tolerance:

Before deciding between fixed and variable rates, honestly evaluate your financial situation:

- How would a 1% rate increase affect your monthly budget?

- Do you have emergency savings to cover higher payments if needed?

- How stable is your income?

- How long do you plan to hold the property or loan?

Remember that the "right" choice varies based on individual circumstances. What works for your neighbour or family member might not be optimal for your situation.

If you already have a variable-rate mortgage and are concerned about rising rates, you have several options:

- Convert to a fixed rate (though current fixed rates may be higher)

- Make lump-sum prepayments while rates are still manageable

- Increase your regular payment amount to build a buffer

- Extend your amortization period to lower payments (if available)

Prime rate forecast and economic indicators

While no one can predict interest rate movements with certainty, understanding the economic indicators that influence the Bank of Canada's decisions can help you anticipate potential prime rate changes.

The Bank of Canada's primary mandate is to keep inflation near its 2% target. When inflation rises significantly above this target, the Bank typically raises rates to cool the economy. When inflation falls below target or economic growth slows, the Bank may lower rates to stimulate activity.

Key economic indicators to watch

Inflation (CPI): The Consumer Price Index is the most important indicator influencing rate decisions. When the annual inflation rate consistently exceeds the 2% target, especially if it's above 3%, the Bank of Canada is more likely to raise rates or keep them unchanged.

Employment Data: Strong job growth and low unemployment can signal an overheating economy that might fuel inflation, potentially leading to rate hikes. Conversely, rising unemployment may prompt rate cuts.

GDP Growth: Robust economic growth may lead to higher rates to prevent overheating, while slowing growth or contraction may trigger rate cuts to stimulate the economy.

Housing Market Activity: Extreme housing market activity (either booming or collapsing) can influence rate decisions, as the Bank considers housing market stability in its policy framework.

Global Economic Factors: International trade tensions, global economic slowdowns, or financial market turbulence can prompt the Bank to adjust rates in response to external pressures.

Current outlook (November 2025)

As of November 2025, most economic forecasts suggest that the Bank of Canada will continue its gradual easing cycle, with potential for additional modest rate cuts in the coming quarters. This outlook is based on:

- Inflation trending closer to the 2% target

- Moderate economic growth

- A stabilizing housing market

- Global economic uncertainties

However, several factors could alter this path:

- A resurgence in inflation

- Stronger-than-expected economic data

- Currency pressures

- Global economic shocks

For borrowers, this suggests that the prime rate may continue its gradual decline, though likely at a measured pace rather than through dramatic cuts.

The hidden costs of prime rate fluctuations

While most discussions about prime rate changes focus on the immediate impact on monthly payments, several less obvious but equally critical financial effects can significantly impact your long-term fiscal health.

Payment allocation shift

When prime rates increase, a larger portion of your variable-rate mortgage payment goes toward interest rather than principal. This creates a "payment allocation shift" that can extend your effective amortization period without you realizing it.

For example, on a $500,000 mortgage with a 25-year amortization, a 1% increase in the prime rate can shift an additional $375 per month from principal to interest. Over five years, this means approximately $22,500 less equity built in your home—money that essentially disappears into interest payments.

This shift can be particularly problematic if you're counting on building equity for future financial plans, such as:

- Downsizing and using equity for retirement

- Accessing equity for children's education

- Using built-up equity for future renovations or investments

Managing the allocation shift: Consider making periodic lump-sum payments directly to your principal when rates increase. Even small additional payments can help offset the slowdown in equity building caused by higher rates.

If you're struggling with this situation, Lotly's secured home loans can help Ontario homeowners restructure their debt to manage cash flow better while protecting built-up equity. By consolidating high-interest debts affected by prime rate increases, you can maintain progress toward your equity-building goals.

Qualification squeeze effect

A little-discussed impact of prime rate increases is what financial advisors call the "qualification squeeze"—when rising rates reduce your borrowing power for future loans or refinancing.

For every 1% increase in the prime rate, your borrowing capacity typically decreases by approximately 10%. This means homeowners who qualified for refinancing or a new mortgage before a rate increase may find themselves unable to qualify afterward, even with the same income and credit score.

This creates a financial trap where those most needing to restructure debt due to higher payments cannot qualify to do so — precisely when they need these options most.

Example of the qualification squeeze: A homeowner with $100,000 annual income might qualify for a $500,000 mortgage at a 4% interest rate. If rates rise to 5%, their maximum qualification drops to approximately $450,000; a $50,000 reduction in borrowing power with no change in their income or credit profile.

Countering the squeeze effect:

- Consider refinancing while you still qualify if rates are trending upward

- Reduce other debt obligations to improve your debt service ratios

- Explore alternative lending options with more flexible qualification criteria

Ready to put your home equity to work? Lotly can help

Understanding the prime rate and its impacts doesn't have to be complicated. With the proper knowledge and strategies, you can navigate changing interest rate environments while keeping your financial goals on track.

Whether rates are rising or falling, your home equity remains a powerful financial tool that can help you manage debt, fund essential projects, or cover major life expenses.

- Take control of high-interest debt by consolidating multiple payments into one manageable monthly payment with Lotly's secured home loan process.

- Access funds quickly and efficiently without the typical roadblocks of traditional banking. Lotly welcomes all credit scores and income types, including self-employed and gig workers.

- Protect your financial future by making strategic decisions about your home equity, especially during periods of prime rate volatility.

- Get personalized solutions that fit your unique financial situation, not one-size-fits-all products that may not address your specific needs.

If you're ready to see your options, Lotly makes it simple by making prime work for you, not against you. Home-equity loans, HELOC strategies, and debt consolidation designed around your real income — benefits, support, contracts, and everything in between. Book a free consultation today to learn more.

The Lotly Team

Our financial writing team at Lotly brings together experts in personal finance to create clear, informative content. With a shared commitment to empowering readers, they specialize in topics such as loan options, debt management, and financial literacy, helping individuals make informed decisions about their financial future. Lotly is part of 8Twelve Mortgage Corporation, FSRA License 13072.