Summary

- Monitor your debt-to-income ratio carefully—when it exceeds 36%, it's time to take action before the situation worsens.

- Create a complete debt inventory to understand exactly what you owe, to whom, and at what interest rates before making any debt management decisions.

- Consider home equity for debt consolidation if you're a homeowner—Lotly's secured home loans can help transform multiple high-interest payments into one manageable monthly obligation.

- Use the hybrid debt repayment approach (combining snowball and avalanche methods) for better psychological and financial results than either method alone.

Watching your debt slowly grow can feel like standing in quicksand—the deeper you sink, the harder it becomes to escape. While some debt is normal in today's economy, the line between manageable obligations and a full-blown debt crisis isn't always clear until you're already struggling.

Recent data shows that total consumer debt in Canada has reached $2.58 trillion, with the average non-mortgage debt per consumer sitting at $22,147. Even more concerning, 1 in 19 non-mortgage holders missed a payment in Q2 2025 — nearly double the rate of mortgage holders.

In this guide, you'll discover:

- 10 clear warning signs that your debt has become excessive

- How to distinguish between healthy and problematic debt levels

- Practical, actionable solutions to regain control of your finances

- Psychological techniques that make debt repayment more successful

By the way, did you know? If you’re seeing these signs in your own finances, and you’re a homeowner, you may be able to consolidate your debts into one manageable monthly payment using your home equity. Lotly specializes in helping Canadians who’ve been turned away by traditional banks find a real path forward — book a free consultation today to learn more.

10 clear warning signs you have too much debt

Debt problems rarely appear overnight. Instead, they develop gradually, often hiding behind seemingly manageable monthly payments until they suddenly become overwhelming. Recognizing these warning signs early can help you take corrective action before a financial emergency strikes.

1. Your debt-to-income ratio exceeds 36%

Your debt-to-income ratio (DTI) is one of the most reliable indicators of financial health. Calculate it by dividing your total monthly debt payments by your gross monthly income, then multiplying by 100 to get a percentage.

For example, if you earn $5,000 monthly and pay $1,900 toward debts (mortgage, car loan, credit cards, etc.), your DTI is 38% ($1,900 ÷ $5,000 × 100 = 38%).

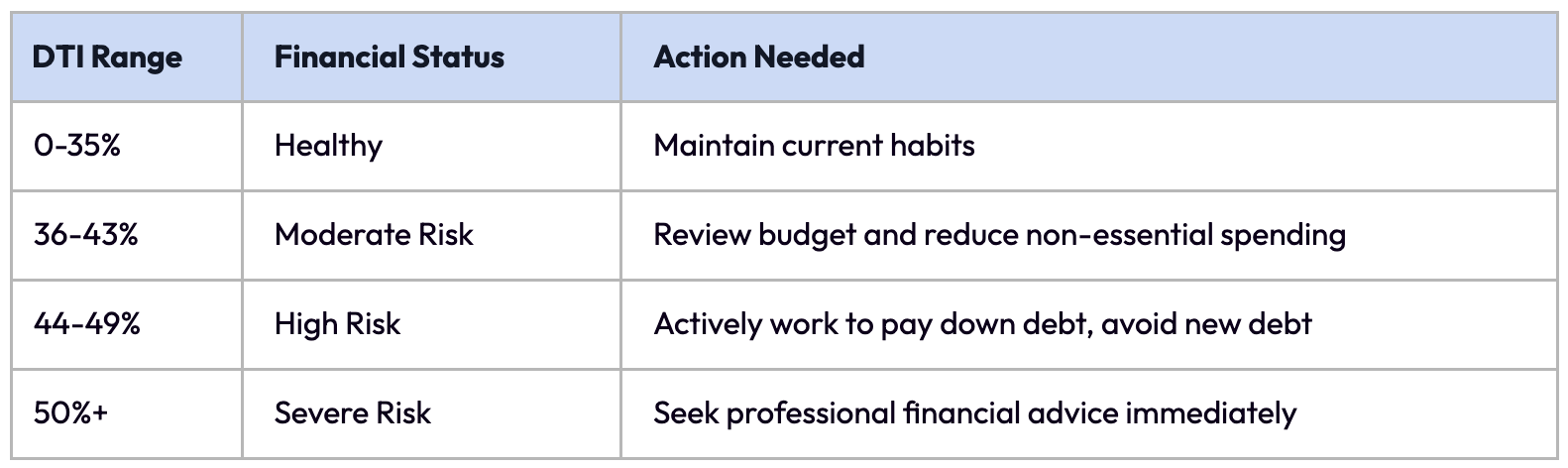

Financial experts generally consider a DTI above 36% to be a warning sign. Here's what different DTI ranges typically indicate:

- 0-35%: Healthy financial position with manageable debt

- 36-43%: Caution zone—debt is becoming burdensome

- 44-49%: Financial stress zone—debt is likely causing significant strain

- 50%+: Financial danger zone—immediate action needed

If your DTI exceeds 36%, lenders see you as increasingly risky, and you'll likely feel the strain in your monthly budget. At this point, it's wise to pause taking on new debt and create a plan to reduce your existing obligations.

2. You can only make minimum payments

When you can only afford minimum payments on credit cards or loans, you're seeing a major red flag. This approach keeps you trapped in a cycle of debt that can last decades.

Consider this: On a $5,000 credit card balance with 19.99% interest, making only minimum payments (typically 2-3% of the balance) would:

- Take over 30 years to pay off completely

- Cost more than $10,000 in interest alone

- Keep you in debt for most of your adult life

Minimum payments are designed to maximize profit for lenders, not to help you become debt-free. If you're unable to pay more than the minimum across multiple accounts, it's a clear sign your debt has become unmanageable.

3. You use credit for necessities

When you regularly reach for credit cards to cover groceries, utility bills, or rent—not for convenience or rewards, but because you lack the cash—you're facing a fundamental budget imbalance.

This pattern creates a dangerous cycle:

- Use credit for essentials because cash is tight

- Make payments on previous credit card charges

- Have even less cash available next month

- Rely even more heavily on credit

Using credit for everyday expenses might seem like a temporary solution, but it signals that your income isn't supporting your basic needs—a clear indicator that your overall debt burden has become excessive.

4. You've maxed out credit cards or credit lines

Having little or no available credit on your cards or lines of credit is both a practical problem and a significant warning sign. When you're consistently at or near your credit limits, you're:

- Likely paying maximum interest charges

- Damaging your credit score (high credit utilization)

- Left without emergency financial options

- Signaling to lenders that you're financially stretched

Credit utilization (the percentage of available credit you're using) ideally should stay below 30%. If you're regularly exceeding 70-80% of your available credit, it indicates you're relying too heavily on borrowed money to maintain your lifestyle.

5. You're being denied for new credit

Rejection for new credit cards, loans, or credit limit increases is the lending industry's way of saying your current debt load is concerning. Lenders have sophisticated algorithms that assess risk, and being denied suggests they've identified potential repayment problems.

Common reasons for credit rejection related to excessive debt include:

- Too many recent credit applications

- High existing debt balances

- Poor payment history on current obligations

- Insufficient income relative to debt obligations

If you're being turned down by mainstream lenders, it's time to step back and reassess your overall financial situation rather than seeking alternative lending sources with less favorable terms.

6. You have no emergency savings

The inability to maintain even a small emergency fund while managing your debt payments is a telling sign of financial strain. Financial experts recommend having 3-6 months of expenses saved, but if you can't set aside even $500-1,000 for unexpected costs, your debt is likely consuming too much of your income.

This creates a vulnerability cycle:

- No savings buffer for emergencies

- Unexpected expense occurs (car repair, medical bill)

- More debt taken on to cover an emergency

- Even less ability to build savings

Breaking this cycle requires addressing the underlying debt burden that's preventing you from establishing financial security.

7. You're experiencing financial anxiety or avoidance

Debt problems often manifest through emotional and psychological symptoms before they completely derail your finances. Watch for these behavioral warning signs:

- Avoiding opening mail or checking account balances

- Feeling anxiety or dread when thinking about money

- Lying to family or friends about spending or debt

- Experiencing sleep problems due to financial worries

- Arguing more frequently about money with your partner

According to FP Canada's 2025 Financial Stress Index, 42% of Canadians say money is their greatest stressor, while 49% lose sleep over financial worries. These psychological signs shouldn't be ignored—they're your mind's way of alerting you to an unsustainable financial situation.

8. You're considering payday loans or cash advances

When you find yourself contemplating payday loans, credit card cash advances, or other high-cost borrowing options, it's a serious red flag. These products typically charge exorbitant interest rates:

- Payday loans: Often 300-500% APR equivalent

- Credit card cash advances: Typically 24-29% APR plus immediate interest accrual and fees

- Pawn shop loans: Usually 20-25% per month (240-300% annually)

Turning to these options indicates you've exhausted more reasonable financing alternatives and are willing to accept extremely unfavorable terms out of desperation—a clear sign your debt situation has become critical.

9. You're receiving collection calls or notices

When accounts have progressed to collections, you're already experiencing significant financial distress. Collection activity indicates you've fallen at least 90-180 days behind on payments, and your creditors have either assigned or sold your debt to collection agencies.

The consequences of having accounts in collections include:

- Significant damage to your credit score (100+ point drops)

- Potential legal action, including wage garnishment

- Continuous contact from collection agencies

- Difficulty obtaining housing, employment, or new credit

Collections represent a late-stage debt warning sign that requires immediate attention and often professional assistance to resolve.

10. You don't know how much you actually owe

Losing track of your total debt is particularly troubling because you can't manage what you don't measure. If you can't quickly determine:

- How many debts you have

- The total amount you owe across all accounts

- What interest rates you're paying

- When each debt will be paid off

Then you've likely lost control of your financial situation. This knowledge gap makes it impossible to create an effective debt management strategy and often leads to missed payments, unnecessary interest charges, and growing balances.

Understanding healthy vs. unhealthy debt levels

Not all debt is problematic. Understanding the difference between healthy financial leverage and dangerous debt levels helps you determine when action is needed and what kind of intervention makes sense for your situation.

What is a healthy debt-to-income ratio?

Your debt-to-income ratio provides a quick snapshot of your financial health. Here's what different DTI ranges typically indicate:

The Bank of Canada considers households with a loan-to-income ratio exceeding 450% or a mortgage debt service ratio exceeding 25% to be at a higher risk of financial distress. These thresholds are important indicators of when debt has become excessive.

Good debt vs. bad debt: Know the difference

Not all debt carries the same risk or impact on your financial health. Understanding the distinction helps you prioritize which debts to address first.

Potentially Beneficial Debt:

- Mortgages (building equity in an appreciating asset)

- Student loans (investing in increased earning potential)

- Business loans (generating income and growth)

- Home equity loans for renovations that increase property value

Problematic Debt:

- High-interest credit cards (especially for discretionary purchases)

- Payday loans and cash advances

- Buy-now-pay-later plans for non-essential items

- Auto loans with extended terms (6-8 years) on depreciating assets

The key difference is whether the debt is building wealth/value or simply financing consumption. Even "good debt" becomes problematic when the total amount becomes unmanageable relative to your income.

Practical solutions for managing excessive debt

If you've identified with several warning signs above, it's time to take action. The good news is that even serious debt problems have solutions. Here's how to start regaining control of your financial situation.

Create a complete debt inventory

You can't solve a problem you don't fully understand. Start by creating a comprehensive list of all your debts:

- Gather recent statements for all loans, credit cards, and other debts

- Create a spreadsheet or use a debt tracking app to record:

- Creditor name

- Current balance

- Interest rate

- Minimum monthly payment

- Payment due date

- Estimated payoff date

- Calculate your total debt amount and total monthly debt payments

- Determine your debt-to-income ratio

This inventory gives you clarity about your complete financial picture and serves as the foundation for your debt reduction strategy.

Develop a realistic budget that prioritizes debt repayment

With a clear understanding of your debt situation, create a budget that maximizes debt repayment while covering essential expenses.

Step 1: Track all income sources. List every source of income, including your primary job, side gigs, benefits, and any other money coming in.

Step 2: Categorize expenses as essential or non-essential.

- Essential: Housing, utilities, food, transportation, insurance, minimum debt payments

- Non-essential: Entertainment, dining out, subscriptions, non-urgent shopping

Step 3: Find areas to cut back.

Look for expenses you can reduce or eliminate temporarily while focusing on debt repayment:

- Subscription services ($10-15 each adds up quickly)

- Dining out (even reducing by 50% can free up hundreds monthly)

- Premium services that could be downgraded

Step 4: Allocate extra funds to debt repayment.

Any money freed up through budgeting should go directly to debt payments, above the required minimums.

Remember that this tighter budget is temporary—the faster you reduce high-interest debt, the sooner you can return to more flexible spending.

Consider debt consolidation options

If you're juggling multiple high-interest debts, consolidation can simplify your finances and potentially lower your interest costs. This approach combines several debts into a single loan with one monthly payment, ideally at a lower interest rate.

For homeowners carrying multiple high-interest debts, consolidation through a secured home loan can provide significant relief. Lotly's secured home loans have helped Ontario homeowners consolidate various debts into a single, more manageable monthly payment, often at a lower overall interest rate.

This approach works particularly well for those who have built equity in their homes but are struggling with credit card debt, personal loans, or other high-interest obligations that are causing financial stress.

How debt consolidation through home equity works:

- Equity Assessment: Start by checking your home's current value minus your mortgage balance to determine available equity.

- Loan Application: Apply for a secured home loan that covers your existing high-interest debts.

- Debt Payoff: When approved, the loan proceeds pay off your existing debts directly.

- Single Payment: Replace multiple payments with one monthly payment, often at a lower interest rate.

For self-employed individuals or those with non-traditional income sources, debt consolidation through traditional banks can be challenging due to rigid income verification requirements. Lotly's secured home loan process accepts various income types—including self-employment, side gigs, and benefits—making debt consolidation accessible to homeowners who might otherwise be turned away despite having substantial equity in their homes.

Explore professional debt management help

Sometimes an objective third party can provide valuable guidance. Credit counseling agencies offer free or low-cost consultations to review your situation and suggest appropriate solutions.

A certified credit counselor can help you:

- Analyze your complete financial situation

- Create a personalized budget

- Negotiate with creditors (sometimes achieving lower interest rates)

- Develop a debt management plan (DMP)

Under a debt management plan, you make a single monthly payment to the counseling agency, which then distributes payments to your creditors according to negotiated terms. This can simplify your finances and potentially reduce interest rates, though it typically requires closing credit accounts and following a strict repayment schedule.

When to consider more serious debt relief options

If your debt-to-income ratio exceeds 50% and you're struggling to make minimum payments despite budget cuts, you may need to consider more significant interventions.

Consumer Proposal: A consumer proposal is a legally binding agreement between you and your creditors, administered by a Licensed Insolvency Trustee. It allows you to:

- Pay back a portion of your debt (often 30-80%)

- Stop interest charges

- Protect assets including your home

- Consolidate all unsecured debts into one monthly payment

Bankruptcy: As a last resort, bankruptcy provides a fresh start when other options aren't viable. While it has serious consequences for your credit (6-7 years on your credit report), it can be appropriate when debt has become completely unmanageable.

Always consult a Licensed Insolvency Trustee before pursuing either option. They're legally required to explain all available debt solutions, not just bankruptcy.

How to rebuild after addressing debt problems

Once you've taken steps to address excessive debt, focus on rebuilding your financial foundation to prevent future problems.

Building an emergency fund to prevent future debt

An emergency fund is your first line of defense against future debt. Even while paying down existing debt, try to set aside a small amount regularly:

- Start small: Aim for $500-1,000 initially

- Automate savings: Set up automatic transfers on payday

- Use windfalls wisely: Allocate tax refunds, bonuses, or gifts to your emergency fund

- Keep it accessible but separate: Use a high-interest savings account that's not linked to your daily banking

Once your high-interest debt is paid off, expand your emergency fund to cover 3-6 months of essential expenses.

Improving your credit score after debt problems

Rebuilding credit takes time, but these steps can accelerate the process:

- Pay all bills on time: Payment history is a major part of your credit score

- Keep credit utilization low: Aim to use less than 30% of available credit

- Don't close old accounts: Length of credit history matters

- Limit new credit applications: Each hard inquiry temporarily lowers your score

- Consider a secured credit card: Use it responsibly to rebuild credit history

Monitor your credit report regularly through free services like Borrowell or Credit Karma to track your progress and ensure accuracy.

Creating sustainable financial habits

Long-term financial health depends on sustainable habits:

- Follow the 50/30/20 rule: Allocate 50% of income to needs, 30% to wants, and 20% to savings and debt repayment

- Practice zero-based budgeting: Give every dollar a job before you receive it

- Implement a 24-hour rule: Wait 24 hours before making non-essential purchases over $100

- Schedule regular financial reviews: Monthly check-ins keep you accountable

- Celebrate milestones: Acknowledge progress to stay motivated

These habits create a foundation for lasting financial stability, helping you avoid returning to problematic debt levels.

Unique debt solutions for different situations

Most debt advice follows conventional wisdom, but research in behavioral economics and financial psychology reveals more effective approaches that combine financial strategy with human psychology.

The debt snowball vs. avalanche method: a hybrid approach

Traditional advice typically recommends either:

- Debt Snowball: Paying the smallest debts first for psychological wins

- Debt Avalanche: Tackling the highest-interest debts first for mathematical savings

However, research with financial psychologists suggests a more effective hybrid approach:

- Start with your smallest debt for a quick win (snowball)

- Then tackle your highest-interest debt (avalanche)

- Return to the snowball method for the remainder

- Set celebration milestones every 90 days

This hybrid approach combines the psychological benefits of the snowball method with the financial efficiency of the avalanche method. Analysis shows this approach leads to 15% higher debt completion rates than either method alone because it provides both early motivation and optimal interest savings.

The "debt-free date" visualization technique

Research from behavioral economics shows that people who establish a specific "debt-free date" and visualize it regularly can significantly improve follow-through on their debt repayment plans. Here's how to implement this powerful technique:

- Calculate your realistic debt-free date:

- Use a debt payoff calculator to determine when you'll be debt-free based on your current payment plan

- Add 10% buffer time to account for unexpected setbacks

- Create visual reminders:

- Mark your debt-free date on calendars (physical and digital)

- Create a visual countdown that you'll see daily

- Use a debt thermometer to track progress

- Establish milestone celebrations:

- Plan small, budget-friendly rewards at 25%, 50%, and 75% progress points

- Share your milestone achievements with a supportive friend or family member

- Use digital tools to track progress:

- Set up automatic payment tracking in apps like YNAB, Mint, or a simple spreadsheet

- Schedule monthly progress reviews

- Implement "future self" journaling:

- Write a letter from your future debt-free self, describing how life feels

- Read this letter when motivation wanes

This psychological approach addresses the emotional aspects of debt repayment that purely financial advice often overlooks, making you significantly more likely to follow through with your plan.

Let Lotly help you take control of your debt

Recognizing the signs of excessive debt is just the first step. Taking action to address the situation is what ultimately leads to financial freedom and peace of mind.

If you're a homeowner with equity in your property, Lotly's secured home loans offer a practical solution for consolidating high-interest debts into one manageable payment. Unlike traditional banks that might reject you based solely on credit score or income type, Lotly considers your complete financial picture.

Key takeaways from this guide:

- Monitor your debt-to-income ratio carefully—when it exceeds 36%, it's time to take action before the situation worsens.

- Create a complete debt inventory to understand exactly what you owe, to whom, and at what interest rates before making any debt management decisions.

- Consider home equity for debt consolidation if you're a homeowner—Lotly's secured home loans can help transform multiple high-interest payments into one manageable monthly obligation.

- Use the hybrid debt repayment approach (combining snowball and avalanche methods) for better psychological and financial results than either method alone.

P.S. If you're ready to explore how a secured home loan could help consolidate your debt and improve your monthly cash flow, Lotly makes it simple. One form, real solutions, and a team that's on your side. Book a free consultation to see how you can get started today.

The Lotly Team

Our financial writing team at Lotly brings together experts in personal finance to create clear, informative content. With a shared commitment to empowering readers, they specialize in topics such as loan options, debt management, and financial literacy, helping individuals make informed decisions about their financial future. Lotly is part of 8Twelve Mortgage Corporation, FSRA License 13072.