- Homebuyers pay closing costs on top of property prices for every real estate transaction.

- Closing costs include provincial and municipal land transfer taxes, legal fees, title searches, property taxes, and administration fees.

- Preconstruction homes and condos require additional closing costs, like development charges and occupancy fees.

- Lotly helps homebuyers alleviate the extra burden of closing costs with down payment assistance.

Shopping for your first home? You’ve probably gone through mortgage pre-approval, bank meetings, and serious saving efforts to make up a down payment.

And once you close the deal, you usually have a couple of months to provide the rest of the down payment and mortgage amount, meaning your closing date might be a month, two, or more after purchase. Hold your horses — you still need to pay for closing costs.

Remember, these are separate from your down payment. Closing costs vary wildly, anywhere from $10,000 to $40,000. And some Ontario residents have been shocked to learn of pre-construction closing charges of over $100,000!

We get it, closing costs are enough to make any homebuyer’s head spin. That’s why at Lotly, we try to alleviate the load with down payment support.

But still, you might wonder:

- What should I budget for closing costs in Ontario?

- How much are closing costs when buying a house, condo, or pre-construction?

- Is there any way to lessen closing costs?

Welcome to Closing Costs 101 — class has started!

What are closing costs?

Closing costs are the extra costs a homebuyer incurs on top of a property price when closing a real estate purchase. Unfortunately, this doesn’t include mortgage insurance (if necessary), down payments, or interest.

Have you ever purchased concert tickets online and felt ripped off by the endless fees at checkout? Closing costs are a similar deal. Admin fees here, registration fees there, and the dreaded land transfer tax all take a heavy toll on your budget. Frustratingly, it’s hard to pinpoint exact numbers for closing costs.

Insurance experts at Canada Life recommend setting aside 3-5% of the purchase price. For example, the closing costs on a $650,000 one-bedroom condo in Etobicoke will run you somewhere between $19,500-$32,500.

It’s especially important to note the biggest fish in the closing costs sea: land transfer tax for both Ontario and Toronto (more on that later).

So what exactly do closing costs entail?

Land transfer tax

You have two types of land transfer tax to manage in Toronto:

- Provincial land transfer tax (Ontario)

- Municipal land transfer tax (Toronto)

It’s not enough to pay for the property. Ontario requires land transfer tax from anyone who “acquires a beneficial interest in land.”

Here’s how you can calculate Ontario land transfer tax using your property price:

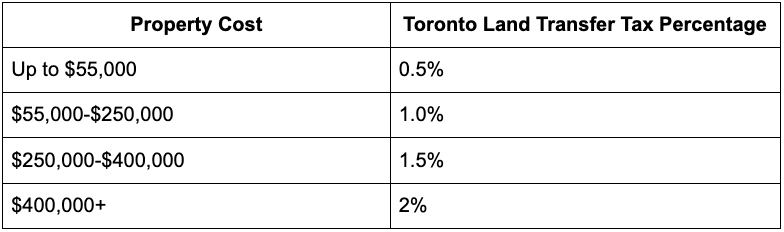

The same goes for municipalities. Toronto’s Municipal Land Transfer Tax (MLTT) has a similarly tiered calculation:

Note: The figures shown are for single-family residences.

You’re responsible for both provincial and municipal land transfer tax. Typically, you’ll split these costs if you purchase your home with a partner. If you’re a first-time homebuyer, however, you could be eligible for a partial or complete land transfer tax refund.

Luckily, Lotly doesn’t leave you on the hook for land transfer tax. We pay our fair share when you obtain down payment assistance from us. We use our 3.5x leverage to cover our portion of land transfer tax for all our homebuyers. For example, if we provide 5% of the 20% down payment, we pay 17.5% (5%×3.5) of the land transfer tax.

Legal fees

Every real estate transaction requires a real estate lawyer’s services. You’ll have to pay them to draft the title deed, compile documents, and take care of various administrative fees. Your lawyer will put together a receipt for you listing all of these costs, usually under separate umbrellas from their own fees (which is typically between $500-$3,000).

Property tax

Some home sellers may have paid the year’s property tax despite selling before year-end. For example, if a seller pays their final annual property tax bill in early autumn and you acquire the home in November, you’ll have to reimburse the seller for some of the property taxes paid.

Deed and mortgage registration fees

Banks charge mortgage registration fees to charge your mortgage to your name. This official registration allows them the legal right to repossess your home if you default on the loan. Mortgage registration fees are typically in the range of $100-$200.

Title search, title insurance, and subsearch

A title search is the legal process where a lawyer researches any other listed names on the property title other than the seller. It’s kind of like a background check revealing any liens or mortgages registered that you don’t know about.

This is one of the most important parts of your closing process. Chances are, it’ll come up clean. But if you skip the title search, you risk some third party trying to reclaim your property!

Title search and subsearch cover the research, while title insurance covers you from any legal costs.

The searches will cost you between $150-$300, while title insurance premiums could add up to $1,000 (one-time fee).

Municipal admin fees

On top of municipal land transfer tax, the City of Toronto will charge you a fee to charge you the tax (weird flex, we know). That will add another $50-$100 to the bill.

Document production

These are often included in your legal fees, but might be charged separately at about $50-90.

Pre-construction closing costs

Closing costs reach a whole new level of bananas if you’re buying a pre-construction house or condo in the GTA.

The annoying part is that it’s difficult to pinpoint figures for these as well. You’ll have to pay the closing costs mentioned above, plus some special, pre-construction-only costs.

Here’s a short breakdown:

- Development charges: These are government levies paid by the developer and passed down to the buyer. RateHub estimates these to max at $4,000; however, one real estate agent cites them as high as $20,000. You can technically establish a cap in your purchase agreement, but the developer doesn’t have to accept it.

- Utility hook-up fees: Pre-constructions are brand new builds, requiring brand new hook-ups to hydro, gas, and water. A modest estimate for these fees would be $500-$2,00 but some homebuyers report builders charging in the tens of thousands for this.

- Assignment fees: Say you purchase a pre-construction with two years left until occupancy. In that time, you might have a change of heart and sell it (assign it to someone else). While developers might have stringent rules for doing so, like prohibiting the listing from large realtor sites, you can usually still manage. Just expect to pay a couple thousand dollars in assignment fees, though. Plus, you’ll have to pay capital gains on any of the appreciation profits.

- Occupancy fees: This is the most unsettling closing cost in the pre-construction world. If your pre-construction is ready for move-in before the title transfer and mortgage registration takes place, you’ll have to pay the equivalent of monthly rent to the developer. This could last as long as a few months to two years.

.png)